What is a cash discount and how is it calculated?

Every entrepreneur is pleased when they see that their customers have paid the invoices made out to them. In order to provide an incentive for this, many service providers and distributors offer a price reduction as a certain percentage of the invoice total. This reduction is called a cash discount.

The situation involves an agreement between the seller and the buyer. The former allows the latter to subtract a specific sum from the agreed-upon invoice amount, as long as the invoice is paid by a specific deadline.

A cash discount is not required by law. It’s simply an offer that a company makes in order to motivate customers to pay faster. In that way, the cash discount is a method for improving sales promotions and liquidity.

Some helpful terms around cash discounts

A cash discount can also be called an early payment discount or prompt payment discount. Although this article has already defined cash discounts above, understanding the concept involves understanding related terms, as well. Here are three terms you should know:

| Discount period | The time a customer is given to pay the invoice and receive the discount before the deadline |

| Discount percentage | The percentage amount that can be deducted from the total invoice amount |

| Cash discount amount | The price reduction that results once the discount percentage has been applied |

Thirty-day-long payment periods are common in the UK. In some exceptional cases, they can even be up to 60 or 90 days. However, in order to provide customers with a more attractive offer, some suppliers and service providers grant cash discounts. The average discount period is 10 days.

There are also graduated discount percentages, in which the discount percentage changes depending on the discount period. In brief, a cash discount is the price reduction that is granted when a customer pays their invoice within a limited time period.

The name, cash discount, may be somewhat confusing when it comes to the payment process. Though cash discounts are granted when the payments are made in cash, they are also granted when payments are made via credit transfer, as long as this happens within the discount period. This means that paying in cash is not required in order to receive a cash discount.

Those who have the opportunity to receive a cash discount should use it, because this strategy allows you to save money without any additional expenditures. That being said, if you have a more tax-efficient means to use this cash, you should choose that option, instead.

Calculating a cash discount

A cash discount is always deducted from the gross amount of the invoice. This reduces the purchase price, which is a significant advantage for the paying business in the transaction. The deductible prior tax is thus also reduced when the cash discount is subtracted.

The cash discount formula is as follows:

- Price of goods: £100

- 10% cash discount (£10)

- Price of goods after discount: £90

- Vat amount: £18 (£90 X 20%)

- Gross invoice total: £108, instead of £120

In the UK, it’s common for the payment period to be 30-days – make sure you double check the individual payment periods, though.

The following example displays the origins of the cash discount example:

An agreement for a cash discount reads: “14 days, 2% discount percentage, 30 days total” (also written as “2/14, Net 30”). This means that if the customer pays the invoice within the first 14 days after the date the invoice was created (in other words, within the discount period), the payment amount in question is reduced by 2%. The customer thus only has to pay 98% of it. If the customer does not make a payment until after the first 14 days are over, however, the customer would need to pay the full invoice amount.

Cash discount modifications are rarely carried out, as the decrease of discount percentages is difficult to impose with respect to the customer. It’s therefore also unlikely that a supplier will raise discount percentages, as this increase is difficult to reverse.

Cash discount and sales price calculation

A sales price calculation is crucial in order for a business to offer its products or services at a price that allows it to make a profit. This calculation naturally has to take the cash discount into account, so that the minimum price limit can be chosen in a way that guarantees the returns exceed the costs. The most popular methods for calculating the list sales price that makes the required profit possible revolve around mark-up pricing. Important calculations in relation to this are the mark-up percentage calculation, and the cost-plus pricing calculation.

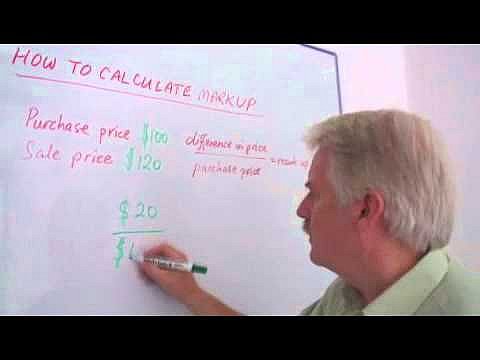

Mark-up percentage calculation

One form of sales price calculation is the mark-up percentage calculation. The mark-up percentage refers to the percentage that is added to the original selling price, so that the business offering a cash discount still makes a profit if the cash discount is used by their customers. You can use the mark-up percentage to arrive at the best sales price, but before you can determine the mark-up percentage, you need to determine the gross profit margin. These calculations will be shown in the following example.

Example: A luxury toy company sells handcrafted music boxes for £100, though they only cost £75 to produce.

- Gross profit margin = sales price – unit cost

In this case, that would mean the gross profit margin = £25 (£100 - £75). This amount can then be used to determine the mark-up percentage.

- Mark-up percentage = gross profit margin / unit cost

The mark-up percentage would then be 0.33% (£25 / £75). Though the sales price was already mentioned in the initial example description, it’s included below to illustrate how the sales price relates to the mark-up percentage.

- Sales price = (cost x mark-up percentage) + cost

- £100 = (£75 x 0.33%) + £75

For another visual representation of this calculation, see the following video. Please note that the video refers to the unit cost as the purchase price, though they’re the same concept for the purposes of the calculation.

To display this video, third-party cookies are required. You can access and change your cookie settings here.

To display this video, third-party cookies are required. You can access and change your cookie settings here.

If you’ve heard of a gross margin before, you may be wondering how this relates to a mark-up. The truth is, they’re different names for the same amount, when it comes to these kinds of calculations. The gross margin is the difference between the sales price and the unit price (in the previous example, this would be £25). Meanwhile, the mark-up is the amount that the unit price is increased in order to reach the sales price (which would again be £25 in the previous example).

How this relates to cash discounts

Once you understand the basic concept of mark-up percentage calculations, you can add the factor of cash discount calculations quite easily. The cash discount affects the sales price, so it’s good to add this factor into all of your calculations. For example, if the company offers a 2% discount, this would amount to £2 of the £100 total sales price. The sales price would then be £98 (£100 – £2), which would shift the gross profit margins and mark-up percentages somewhat.

- Gross profit margin = £98 – £75 = £23

- Mark-up percentage = £23/£75 = 0.31%

Of course, it’s also important to keep in mind that this is a simplified rendering of the mark-up percentage calculation. It does not take into account all of the indirect costs that could apply in a real-life scenario, and is instead meant as an overview.

Cost-plus pricing calculation

An alternative to the mark-up percentage calculation is the cost-plus pricing calculation. It’s characterised by the inclusion of various costs related to the production of a product: the direct material cost, direct labour cost, and overhead cost. The mark-up percentage is then added to these costs, in order to arrive at the sales price. Before working out an example of this formula, it’s necessary to understand what its parts mean.

While the mark-up percentage was described in the previous section, the other three parts have not yet been discussed. The direct material cost refers to the physical elements that go into creating the product, such as wood and paint on the case of the music box, and the mechanism inside it. The direct labour cost refers to the financial value given to the work it took to create the box, such as the woodworking, painting, and creation and insertion of the music box. Finally, the overhead costs are derived from considering the extra costs of the manufacturing process, such as the cost of rent and utilities in the factory where the music boxes are made. Once you understand those costs, it’s time to put them together into the cost-plus formula:

- Sales price = (direct material costs + variable costs + direct labour costs + overhead costs) x (1 + mark-up percentage)

- If the direct material costs are £45, the direct labour costs are £13, and the overhead costs are £18, while the mark-up percentage remains 0.31% after the cash discount has been taken into account, then the sales price would be:

- Sales price = (£45 + £13 + £18) x (1+ 0.31%) = £99.56, rounded to £100

In the end, the mark-up percentage calculation and the cost-plus calculation are simply two strategies for determining which sales price would be best.

Trade discount vs. cash discount

It’s common to mistake a cash discount for a cash discount. While a trade discount is subtracted from the list price, calculating the cash discount shouldn’t happen until the final invoice sum has been determined. The cash discount is only subtracted from the payment amount if it’s made use of within the discount period, while a trade discount is not dependent on the payment deadline and is taken into account immediately.

Furthermore, a trade discount depends on the quantity of goods purchased or amount of purchases made, while a cash discount is (as previously described) based on the time period when the payment is made. Here is an example of a trade discount: A seller charges £0.95 per product for the purchase of 100 products, and only £0.89 per product for a purchase of 200 or more products. Cash discounts, on the other hand, are granted independently of the quantity of products purchased.

A trade discount is a guaranteed reduction of the list sales price, while a cash discount is an optional reduction of the final invoice sum.

The following table shows a comparison between a cash discount:

| Cash discount | Trade discount |

| Price reduction with a deadline, independent of the quantity of products purchased | Reduction dependent on purchased product quantity or the amount of purchases made |

| Subtracted from the gross amount (with sales tax) | Subtracted from the net amount (without sales tax) |

| A price reduction that is granted retroactively | A previously agreed upon and guaranteed price reduction |

The difference between customer and supplier cash discounts

A customer cash discount is being referred to when a business grants its customers a cash discount. This cash discount represents a cost element for the business and thus needs to be taken into account when making a sales price calculation.

When the supplier grants the business a cash discount, it’s a supplier cash discount example. This discount makes a reduction of the purchasing costs possible.

To determine whether making use of the cash discount is worth it, you should first calculate the effective interest rate of a supplier credit and compare it to the bank’s lending rates. The effective interest rate for a supplier credit is calculated with the following formula:

- Discount percentage / (1 – discount percentage) x [360 / (full allowed payment days - discount days)]

- Example: 2% cash discount when payment is made within 3 days, or net 30 days

- 2 / (1 – 2%) x [360 / (30 – 3)] = 27.19% effective interest rate for the supplier credit

If the calculated interest rate is greater than the bank’s lending rates, it’s advisable to take out a short-term loan from a bank in order to finance the utilisation of the cash discount.

Why it’s highly advisable to use cash discounts

Making use of the cash discount is beneficial, even if it often only saves a few pounds. The cash discount has several advantages for both customers and suppliers.

Advantage for the supplier

The fact that the invoice is paid more quickly by the customer, means that the supplier can address their payment obligations more quickly, too. The supplier can also use cash discounts to offset possible cash shortages, by arranging a temporary increase of the cash discount. The losses caused by the temporary increase of the cash discount are negligible compared to the costs that could arise from cash shortages.

Advantage for the customer

Calculated over the course of a year, making use of cash discounts can save a relatively large amount of money. As the previous example shows, it’s sometimes even worth it to take out a loan from a bank in order to use a cash discount. As long as the effective interest rate for the supplier credit is greater than the interest rate for the bank’s loan, taking on a loan is more cost-efficient.

Comparison with loan interest rates

In some cases it can be quite advisable to take out a short-term loan in order to make use of the supplier’s cash discount – not only as a seller, but also as a private individual. However, the situation should first be analysed, as it’s possible that the bank’s interest rates are so high that taking out a loan is not worth it.

Example:

The invoice amount that needs to be paid totals £5,000. If the invoice is paid within the first 10 days after the invoice has been received, the customer can deduct a 2% cash discount.

Is it advisable to take out a loan in order to make use of the cash discount?

| Cash discount | Bank loan |

| Cash discount: Forgoing the cash discount deduction from your account (= cost of the supplier credit) 2% of £5,000 | (Premature payment with a deduction of the cash discount and savings of £100) (taking on a bank loan for 20 days – 10% annual interest rate) C = costs, p = percentage, d = days Z = C*p*d 100*360 Z = 4.900*10*20 100*360 |

| Totals = £100 | Totals = £27.22 |

Profit from making use of the cash discount → £100 - £27.22 = £72.78

A bank loan is often cheaper than a supplier credit, although it’s always necessary to analyse the situation yourself in each case to be sure.

If no cash discount is mentioned in the invoice, it’s sometimes worth it to inquire about one. Businesses are generally very accommodating and allow the cash discount to be listed separately on the invoice.

Please note the legal disclaimer relating to this article.

Reviewer

Anne-Laure Wolber

Anne-Laure has been part of the IONOS Digital Guide since its inception in 2016. As an expert in the startup category, she focuses primarily on the strategic integration of SEO, GEO and conversion rate optimisation. Over the years, she has also gained extensive experience in related performance disciplines such as lead generation and native advertising. As a polyglot, she leverages her multilingual background to develop content strategies with precision and impact for international audiences.